Visa: Hidden In Plain Sight

It's called Visa because your credit card is like your "Visa" into any store!

A bit more than a week ago, Visa and Mastercard reached an agreement with a group of merchants to reduce interchange rates as well as cap them at an agreed upon rate. The settlement includes various other provisions, such as allowing groups of merchants to form negotiating committees and surcharging at the brand level (Visa & Mastercard).

Under the settlement, Visa and Mastercard would reduce swipe rates by at least four basis points - 0.04 percentage points - for three years, and ensure an average rate that is seven basis points below the current average for five years. Both card networks also agreed to cap rates for five years and remove anti-steering provisions.

Most small and medium sized businesses report their highest non-labor operating cost to be these “swipe fees”. Merchants are forced to pass these fees on to customers, meaning the average American family eats up more than $1,000 a year in credit-card fees. Luckily the lawsuit has brought some relief. Visa estimates that these reductions accumulate around $30 billion in cost savings over the next 5 years.

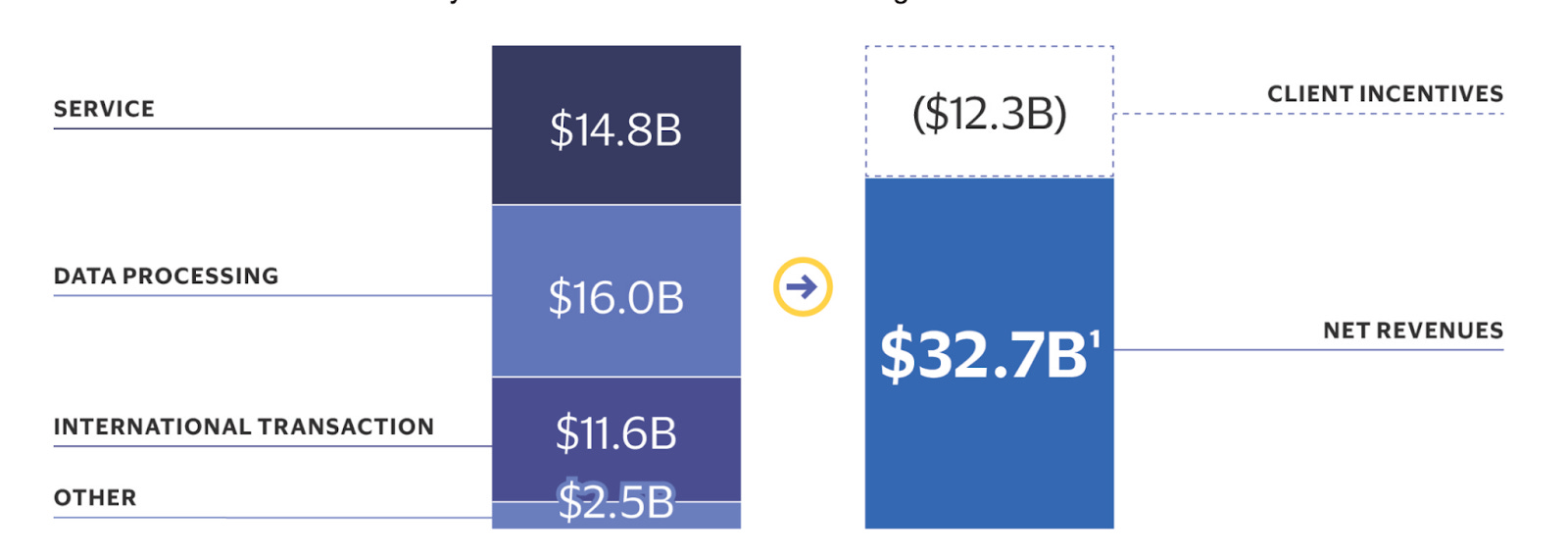

$30 billion over 5 years - that’s around $6 billion a year! Visa makes money by processing payments between merchants and customers using its network. With Visa processing nearly 4 out of every 10 transactions globally, doesn’t that mean Visa stands to lose out on ~$2.5 billion? In 2023, the payments giant reported $32.7 billion in net revenues, up 11% from last year. Here’s the breakdown of how revenue looked in Visa’s most recent fiscal year.

Image 1 - Visa FY 2023 10-K Revenue Segmentation

Remember our video about Visa from a while ago - “The Company With 100% Margins”? Well, that’s surely true the way that Visa reports revenue. A quick glance at their Income Statement from 2023 shows a reported $32,653 with absolutely no cost of goods sold. You’ll find that in the image below and the one above. Hold on…why is there an extra $12.3 billion in the first picture? To answer this question , let’s rewind back to the company’s roots.

Image 2 - Visa FY 2023 10-K Net Revenues

BankAmericard

You see, in 1968 Visa’s predecessor - BankAmericard - was in some hot water. First launched in Fresno in September of 1958, Bank of America (B of A) soon proliferated the issuance of their BankAmericard program, reaching well over 2 million in just a year. Soon after, the BankAmericard program expanded past California in an effort to compete with another network, Interbank/Master Charge.

But with no technology, how did any of this function? Basically, merchants like your local corner store would put up a sign that they accept BankAmericard. When a customer comes up to use their BankAmericard, it would essentially be a sign that they are “good for their money”.

As a merchant, you would have assurance that you can go to your bank, present them with these tallies (called sales drafts) and get your discounted rate on the dollar. Then these merchant banks, “acquiring banks”, would invoice all consumer banks to recoup their expenses.

Think about the leg work for these banks! Pretty quickly, this whole reconciliation and invoicing operation became massive overhead. It did not take long for any bank at the time to realize…B of A does not really need to do anything except just issue these cards, but somehow collect a modest fee while doing literally no legwork to enable the network.

The franchisees complained and B of A hesitantly put together a committee to figure out what was going on here. Little did they know, this committee would soon convince them to break off the entire BankAmericard program, led by Dee Hock.

Dee Hock’s Stroke Of Genius

Most people do not know who Dee Hock is. Born in rural Utah, Dee Hock wasn’t a superstar banker, if anything he was the opposite. In 1966, Dee was running the BankAmericard franchisee program at the National Bank of Commerce, one of the first banks to issue the credit card.

1969 was Dee’s time to shine. While all the other bank managers were mindlessly lining up to fight B of A, Dee realized that the real solution was to make this BankAmericard program a separate company, not owned by a bank. And that’s exactly what happened. Dee walked into a meeting with B of A executives and pitched to them that a fraction of a separate network would be magnitudes more valuable than the network that B of A was trying to build. Guess what - he was successful!

Convincing B of A was monumental, but Dee still had to get all these state franchisee banks on board. At the time, federal regulation made it illegal for banks to operate over state lines, which meant 3 times more banks today than were in the 70s! To get these banks on board, Visa had to make the whole system somewhat of an equitable meritocracy.

To make it work, Dee required that Visa operate as a for profit, non stock corporation. That’s right, Visa did not issue stock into its company in a traditional sense. Rather, the share of profits that a participating bank would receive would be determined by the amount of volume they brought to the network. For example, if I brought in 5% of the total volume in the network, I would be entitled to 5% of the profits from merchants and consumers.

Banks immediately loved this idea. Not to say it did not require immense persuasion, but Dee was able to sell the same vision he sold Bank of America. A part of the Visa network would be leagues more valuable than any single network by one bank. That brings us back to that runaway $12.3 billion from Visa’s revenue, classified as “Client Incentives”.

Client incentives, which are earned by the clients, are primarily tied to payments volume including cross-border payments volume, processed transactions and number of cards.

VisaNet

"Money had become nothing but alphanumeric data recorded on valueless paper and metal.”

Dee Hock long knew that money was nothing but a way of keeping a tally of what you had and what others had. He knew that the best way of extracting money was not what the banks were doing - lending, issuing mortgages, and whatnot. Rather, the real way to extract value in money was to provide a seamless way to exchange it. If Visa could be instrumental in the exchange of money, the possibilities are endless.

Luckily for Visa, BASE I was introduced in 1973 - meaning real time authorization and clearing of transactions. Over the past 30 years, this network of authorization and clearing morphed into VisaNet. Within a matter of seconds, merchants are able to tap into VisaNet to authorize transactions.

Today, Visa and even Mastercard are able to settle with merchants for lower interchange fees because they already profit unimaginable margins over any other company. As long as spending increases, Visa can maintain its dominance over a payment network simply by making sure the next merchant that opens uses Visa. And why wouldn’t they?

That’s all for this one folks! If you enjoyed reading, please feel free to share with your friends. Reach out to us at logicallyanswered@substack.com if you have any insider opinions or leave a comment on our Substack page!

Interesting, never heard of the full story, but still insightful.