Payments May Have Become A Commodity

Stripe used 7 lines of code to become a $100 billion company

Have y’all noticed the amount of companies in the payments industry recently? You’re probably quite acquainted with using Venmo, CashApp, Zelle, and PayPal when paying your friends or even at some small mom-and-pop shops. Or maybe you have used Plaid, Synapse, or Yodlee when linking your bank account to move your money. In the online and physical point-of-sale (POS) space, there has recently been a boom in the number of companies that offer payments solutions. PayPal, Square (Block), Braintree, Verifone, Clover, Ingenico, Toast, Adyen and Stripe.

Kind of like in high school, there are cliques in the payments space. PayPal, Square, and Stripe operate as a payment aggregator. Traditionally, if you were to run a store selling coffee for example, to accept payments at your store, you’d need to go through a cumbersome process of disclosing a ton of information to receive a merchant ID (MID). Then you can employ a platform such as Verifone or Ingenico to physically accept the payment at the register.

But all of that has changed with PayPal, Square, and Stripe - the focus of today’s piece. These companies came along with a payment aggregator model that circumvents the traditional process of getting an MID and instead uses the MID provided by the payments platform. In return, these companies take a cut of each transaction processed. Stripe’s cut is currently 2.9% + 30¢ for each successful card charge.

This business model drew massive attention to the payments space. Stripe has largely focused on the online crowd - but Square, Toast, and Clover quickly spun up to modernize the physical POS space. You’ve probably seen one of these Verifone readers - take a look at how they’ve had to catch-up to the competitors.

Anyways, who even cares about what brick-and-mortar does nowadays. The future is online, and there’s one player that’s turning peoples heads.

Journey To Success

Here’s a line from Stripe’s recent annual letter:

Charlie Munger described a two-part rule that works wonders in business, science, and elsewhere: 1) take a simple idea and 2) take it very seriously

If you’re a developer tasked with building out a checkout portal at the time, the project was rather monumental. Think about the numerous ways someone can choose to pay. PayPal, credit card, debit card, cryptocurrency, and payments rails are a few - but in reality you need to be able to accept as many as possible.

So John and Patrick sold simplicity to the market that felt the pain. Actual companies could care less - but the developers that worked for them sure as hell cared.

With Stripe, all a startup had to do was add seven lines of code to its site to handle payments: What once took weeks was now a cut-and-paste job.

Well, this is kind of an elementary explanation of what actually happened. On top of a simple cut-and-paste, Stripe offered a modern UI and excellent documentation for developers. Revenue operations benefitted too. Stripe did not come with the baggage of frozen funds and unavailable revenue that many small businesses complained about PayPal. If you want a better picture without all the glazing, check this out.

Again, what’s amazing with Stripe is that they aren’t doing anything innovative. They aren’t building out a blockchain network or creating a global payments rail. At the core of their business is simplicity for developers - create an option that's just so easy to integrate and companies will choose it over PayPal, Braintree, or whatever the next payments startup is.

Underneath all these qualifiable advantages that Stripe offered existed a spillover effect from making things easier for developers. And this is the exact problem Stripe is trying to solve. The Collision brothers mention it often - online payments are ultimately a conversion optimization problem. Given the playing field is the internet, the solution to this optimization problem is in the details. Even nuances like UI optimization can increase conversion by 3%.

Stripe went deep on payments for a long time. When it came to adding products to the lineup, the decision really came down to - does the product improve the conversion our customers are trying to optimize? Think back to our newsletter on Nvidia. Jensen was keen on a first principles approach and Stripe’s first principles boiled down to solving the conversion optimization problem.

Their first new product - Connect - was all about minimizing friction. Connect offers end-to-end embedded solutions that companies can use to sign people up, accept payments, and manage end user accounts. But on top of all of that, Connect could be used to pay out third parties, something that Booking.com for example has used to pay out the airlines or hotels that you select on their platform. Stripe Billing, Issuing, and Treasury all built around payments as a core to complete the entire financial stack for any company.

Warren Buffett Moment

Warren Buffett says that Berkshire’s goal when looking for a business is to find one “with a wide and long lasting moat around it protecting a terrific economic castle with an honest lord in charge of the castle…in essence that's what business is all about”. He goes on to say that most moats are useless, but that’s expected in a capitalistic society. It’s our job as a critic walking by to ask why the castle is standing up and what’s going to keep it standing or cause it to fall in 5, 10, or 30 years from now.

When evaluating a company's moat, Warren says it boils down to these:

Switching Costs

Agency Costs

Economies Of Scale

Position In Consumers Mind (Brand)

Permanence (Are they here to stay?)

Dependence On Leadership

All castles fall eventually, so the key factor in determining when is to assess how strong they are. How strong is Stripe’s castle? As far as those other companies mentioned - PayPal, Braintree, Square, Adyen, Plaid…the list can realistically go on much longer…is it fair to lump Stripe in with them?

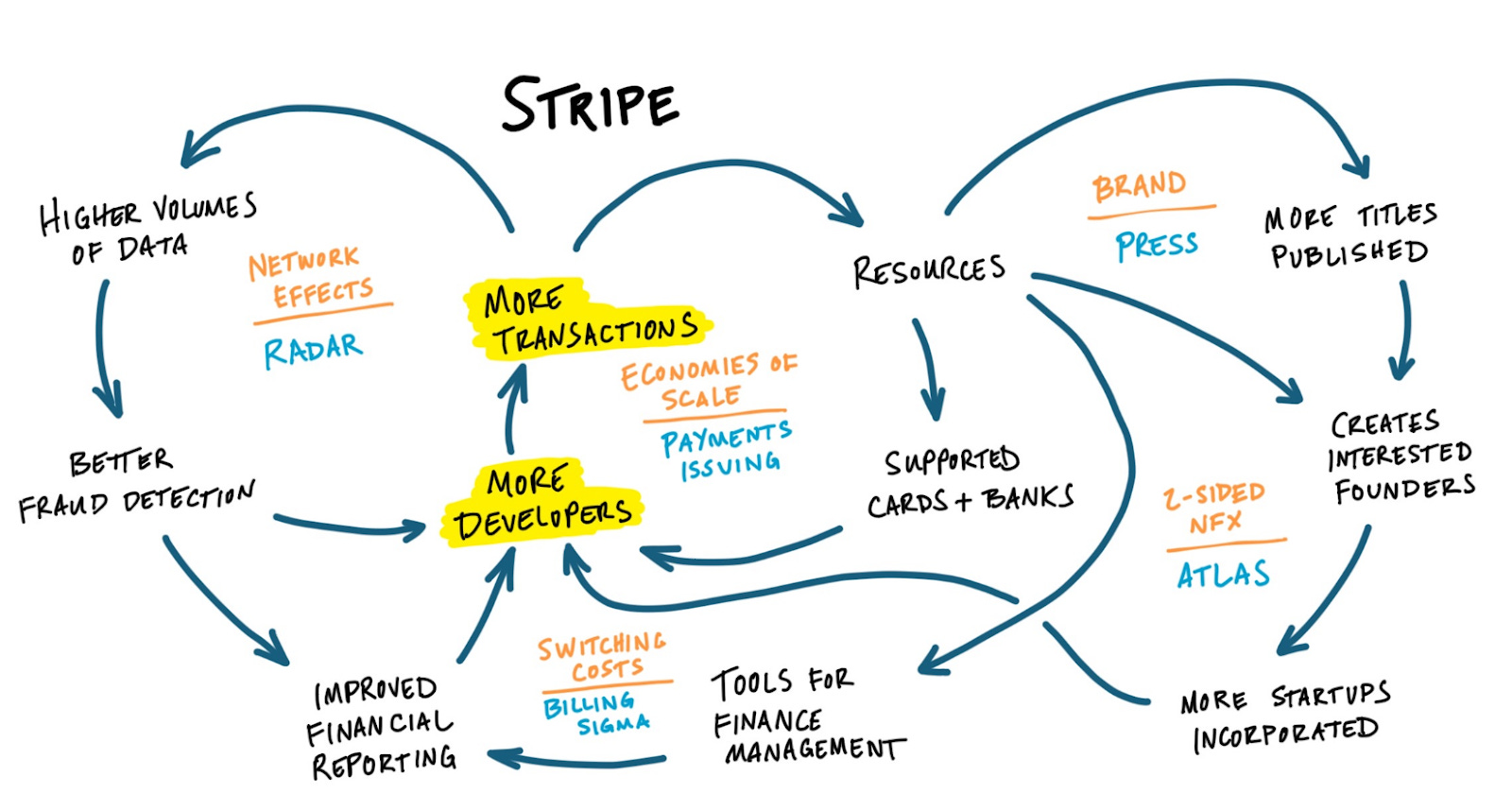

It is fair to say Stripe does not want to be seen as a competitor to any of these companies. The company’s vision is literally to “grow the GDP of the internet”. How do they do this? This value flywheel courtesy of Coleman McCormick summarizes it best:

Many of Stripe’s competitors are one dimensional. Plaid can help link banks with a platform, Experian can help detect fraud, PayPal can offer payments services, and LegalZoom can help you incorporate, but none of them currently do all - and for the foreseeable future, won’t!

Simply because Stripe is becoming the new Visa. Whereas Visa was the bridge troll of the physical credit card scene, Stripe is becoming the bridge troll of the online payments space by inserting themselves in every checkout page on the internet. With IPO rumors on the rise, it’s worth noting the financial position of the company. Stripe crossed $1 trillion in payments in 2023 with 10% of the volume being driven by 100 customers. It looks like economies of scale are starting to kick in, making them a force to reckon with in the future.

That’s all for this one folks! If you’re interested in more content breaking down the world of payments, let me know by liking this post or dropping a comment. If you enjoyed reading, please feel free to share with your friends. Reach out to us by replying to this email if you have any insider takes or leave a comment on our Substack page!

Thumbnail from Wikipedia

{kind=link}