Apple Went On A Shopping Spree (On Itself)

The $2.8 trillion giant may be struggling understand its role in the future of tech

As a channel that grounds itself in covering the rise and fall of companies and other technology content, one trait that almost each and every one of these companies share is that they trade on the public markets. They elect to make their stock available to trade on public exchanges, which means (barring regulation), each and every one of you can go trade Apple, Facebook, Airbnb, Uber, you name it.

In exchange for accepting money from the general public - companies are subject to a few restrictions from regulators like the SEC. The SEC mandates that companies file quarterly and annual financial statements and other mandatory documents like when someone sells a large portion or buys a large portion of their stock.

Quick tangent here: do people actually read these filings? The data shows that in a raw sense, not really. Looking at data from the EDGAR website (database with all annual reports), the average company only gets around an average of 28.4 requests for a given report.

$46.2 trillion in overall market capitalization over US equity markets and only 28 requests?! Bottom line, it does not look like investors are sitting on their hands without any information - what’s actually being played here is a large-scale game of telephone. Apple releases some information, a few key people download and process it, some of them get on CNBC and tell the world about it, others pass it down the chain to analysts, financial influencers, and so on. Eventually, this information gets fully parsed down and provided to the interested American in a digestible manner.

I think that’s enough of a tangent - bottom line, every quarter, every public company is expected to report how they did and what they plan to do in the future. Prior to this earnings release, analysts release what they expect the company to do in terms of earnings per share (EPS), revenue, or profit. Analysts use a combination of forecasting models, guidance from the company, and macroeconomic factors to come up with a fair estimate for how the company should do.

Over the years, this earnings event has actually led to a lot of issues because of something called the “Principal-Agent Problem”. You see, C-Suite positions are theoretically elected by the shareholders when they get appointed by the board of directors. So, if you’re a CEO and wanna keep your job - you better keep increasing those revenue and profit numbers! This incentive plan motivates those at the helm of companies to engage in a wide variety of schemes to keep their company afloat.

Apple In The News

All of this brings us to Apple’s earnings last week - the company reported a drop of $7 billion in product revenue since the same time last year and an even steeper 30% drop over the past quarter. EPS of $1.51 was beat by a slight 2 cents.

Buffett also announced that Berkshire is planning on dumping 13% of their Apple Stake, skinning it down to $135.4 billion. Yes, yes it's still quite large, and still easily casts a large shadow over Berkshire’s second largest investment.

Given all these headwinds, it looks like the future is pretty bleak for Apple. So why is the stock up since earnings?

Apple increased its cash dividend by 4% and authorized an additional program to buy back $110 billion of stock. The buyback is the largest in the company's history.

One-Hundred and Ten BILLION. Not only is this buyback the largest in the company’s history, it's the largest ever in corporate history. In fact, this single buyback is larger than most companies on the biggest exchange in London. Since 2008, Apple’s share repurchases have totaled more than $800 billion, setting the top 5 spots on the list.

Why in the world is the company spending entire nation GDPs just to buy back stock? A buyback as large as this one puts into question Apple’s long-term vision. Is this purely just a play to buy back shares or is there something more dark looming in the background?

Understanding Buybacks

If you’re ever wondering what it is the CEO or CFO does, Michael Maubossin breaks it down well here.

The primary goal of a management team is to invest financial, physical, and human capital at a rate in excess of the opportunity cost of capital.

This is a very academic way to put it, but Michael’s basically saying that when it comes to making decisions on where to invest money - the most optimal decision is the one with the highest possible rate of return over the cost of capital (cost to finance your business).

Ultimately, responsibility of the management team is to maximize long-term value for ongoing shareholders. Is all of this good for the long-term shareholder?

Companies could invest money into R&D and product development, capital expenditures to build up new factories, or even towards buying other companies. If Apple is out here spending $110 billion on buybacks - is that a sign that they don’t have a higher yielding project? Well, here’s how share buybacks add value to the stakeholders:

A share buyback is when a company uses its money to buy shares of its own stock. This effectively removes those shares from the market, reducing the total number of outstanding shares in the company. Since there are fewer shares on the market, it should theoretically make the remaining shares more valuable.

This is similar to a dividend. If Apple buys back 4% of the company and shares theoretically become more valuable just from a supply/demand basis. Since there are less shares, each share also receives a higher dividend.

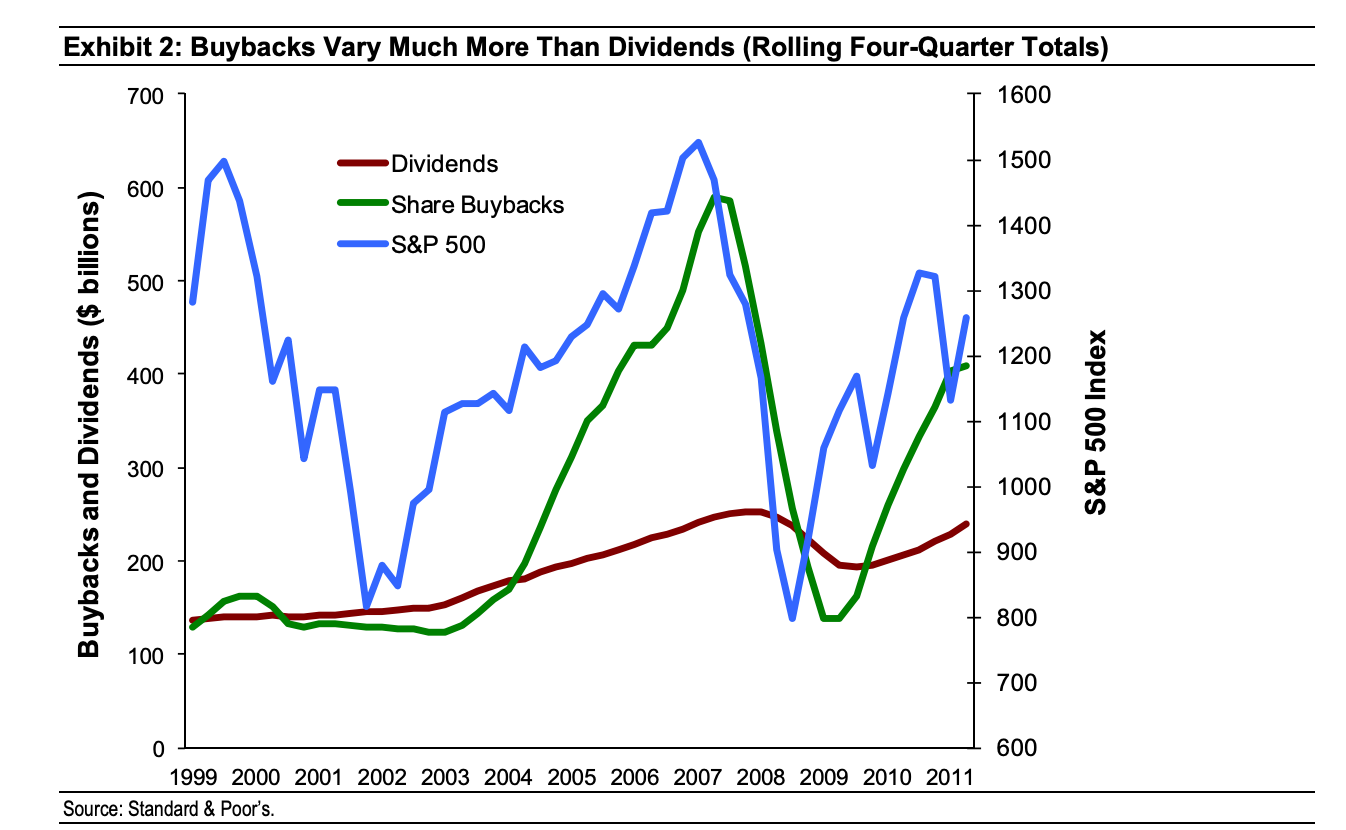

Here’s another neat statistic that displays how an index is generally affected by a buyback. Share buybacks tend to follow the index in a lagging sort of way. Buybacks increase after the market already peaked, meaning a surge of buybacks could actually be a red flag for Apple itself and the overall market.

So is Apple using buybacks to compensate for declining fundamentals? On the bright side, Apple did mention that is recorded revenues in 12 countries including India, Spain, and the Middle East. Also, the value in services still remains. Services revenue increased by more than 14% YoY which is showing a slow shift away from the pure hardware play we’ve been used to.

In reality, it will take a bit longer to tell if Apple has started to wave the white flag on the business. WWDC is coming up and the Vision Pro, while in the graveyard for now, is still an unfinished product. The management team sure looks like they are stuck between a rock and a hard place. Through buying back shares and upping the dividend, the company is pulling accounting levers to increase shareholder returns - not innovation. Sign that Apple is headed into the background.

That’s all for this one folks! As we develop the newsletter, I’ll try to expand the diversity of topics and angles we cover. If you’re interested in more content about how companies take advantage of accounting levers to maintain stock performance, let me know by dropping a comment or liking this post. If you enjoyed reading, please feel free to share with your friends. Reach out to us at logicallyanswered@substack.com if you have any insider opinions or leave a comment on our Substack page!

Very interesting update. Thank you!

why doesn't apple invest in other tech service companies like Tencent